NAIFA President-Elect John Wheeler, CFP, CLU, ChFC, CRPC, LUTCF, CLTC, LACP, CPFA, is a contributor in a recent issue of the CSA Journal, the publication of the Society of Certified Senior Advisors. In the article, “Funding Solutions for the Longevity Economy—Financial Security for Longer Lives,” John shares why true financial planning goes far beyond investments or retirement income alone.

1 min read

John Wheeler Featured in CSA Journal on the Power of Holistic Planning

.png)

Topics: Retirement Planning

2 min read

Why Future-Ready Planning Can’t Wait

NAIFA's Carroll Golden recently shared a striking insight that should give every financial professional pause. According to new Pew Research, Americans are three times more likely to say they would prefer to live in the past rather than the future. Only 14% chose the future.

Topics: Retirement Planning #NAIFAProud Retirement

4 min read

Considering Medicare Costs in Retirement Planning: What Financial Professionals Need to Know

For many Americans, reaching Medicare eligibility marks a noticeable decrease in healthcare spending. Of course, that doesn’t mean that Medicare is free. For financial advisors helping clients prepare for retirement, understanding and planning for the costs associated with Medicare is critical. While these costs are often lower than those incurred through pre-65 health insurance, they remain significant, especially when viewed over a multi-decade retirement.

Topics: Retirement Planning Medicare Medicare Part D

2 min read

FSP Offers Professional Learning Resource on Retirement Planning

.png)

Retirement Plans and Retirement Planning, a newly revised ebook by Kenn B. Tacchino, JD, LLM, Professor of Taxation and Financial Planning at Widener University, is a valuable resource for financial planning students and practitioners. The book is published by FSP, a NAIFA Community, and Professor Tacchino is editor of FSP's Journal of Financial Service Professionals, which NAIFA members may access online as an educational benefit.

Topics: Retirement Planning Professional Development

3 min read

The IRA Is 50 This Month!

Advisor Today Guest Column

January of 2025 is the 50th anniversary to one of the most important pieces of legislation in the retirement planning arena ever put into law by Congress. What I’m referring to is the enactment of ERISA, the Employee Retirement Income Security Act. Without question, ERISA brought about significant changes during the second half of the twentieth century. The key component to ERISA, which became law on January 1, 1975, was the establishment of the Individual Retirement Account or IRA. And what a monumental impact IRAs have had on the retirement planning market from that day forward. According to recent data, approximately 55 million Americans (representing around 42% of all households) hold IRAs with the average balance being around $195,000 per taxpayer.

Topics: Retirement Planning

1 min read

What You Don't Know About Social Security Can Hurt You ... And Your Clients

Thomas Drapala, RSSA, is Director of Strategic Partnerships, Registered Social Security Analysts, and a passionate advisor and educator with deep expertise in Social Security. He is also a keynote speaker at NAIFA's Apex, September 19-21, at the Arizona Biltmore.

Topics: Retirement Planning Apex

1 min read

Social Security: Will It Still Be There?

.png)

In the ever-evolving landscape of retirement planning, Social Security remains a critical source of income for most Americans. The annual release of the Trust Fund Report, issued in May, sparked widespread media coverage and client concern. Questions such as "Will Social Security still be there?" and "Is it going broke?" continue to circulate. Join us for a webinar on Wednesday, June 26, 2024, from 12:00 pm to 1:00 pm Eastern, sponsored by Security Mutual Life which can help you deal with the concerns that clients may have.

Topics: Retirement Planning Retirement

2 min read

Americans Want Guaranteed Lifetime Income Products

A new study from the American Council of Life Insurers (ACLI) shows an increased interest in annuities amid growing economic uncertainty.

The study, which surveyed more than 1,000 Americans between the ages of 45 and 65, found that 54% of respondents are considering “a guaranteed lifetime income product that pays out like a pension.” This trend held among all income brackets, with the greatest interest among minority communities, including Black and Hispanic respondents and those who identified as "other." The survey also found that 91% of respondents would prefer to work with a financial professional who offers products and services that meet their needs.

Topics: Retirement Planning Retirement Legislation & Regulations Research/Trends

2 min read

Mastering Retirement Income: Decumulation Diversification Strategies Revealed

.png)

If you are concerned about diversifying your clients' income during retirement and are searching for strategies to protect against potential increases in taxes and inflation, then join the next Advisor Today webinar on Thursday, June 22 at 2 pm eastern with Allianz.

At "Decumulation Diversification," Schyler Adams, Director of Advanced Strategies & Planning Platforms will reveal concepts and innovative approaches to secure your clients' financial future. Don't miss this opportunity to optimize retirement income and help your clients achieve long-term financial stability.

Topics: Retirement Planning Financial Planning Retirement Webinar Advisor Today

2 min read

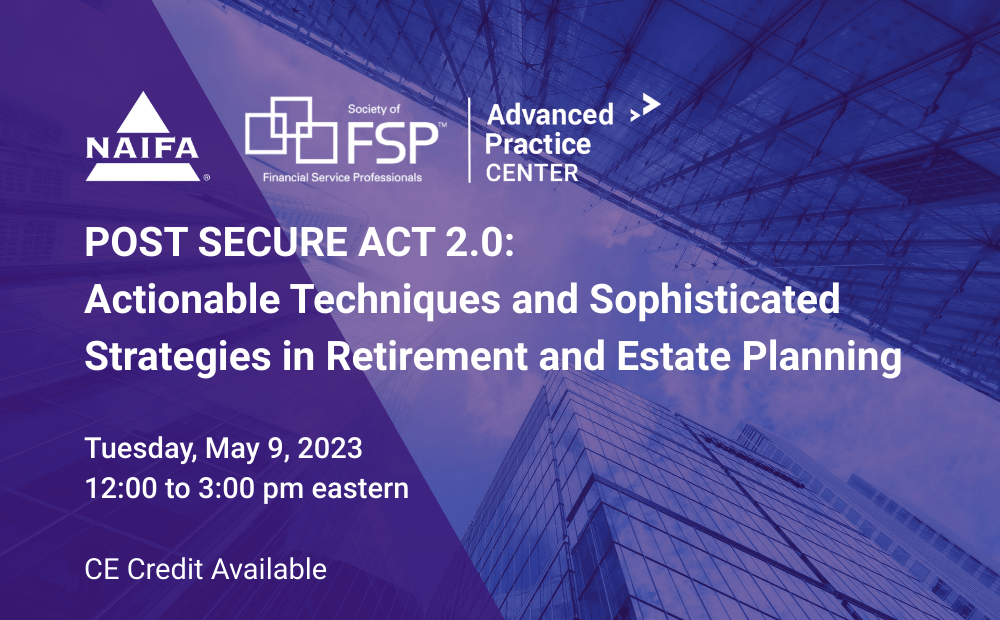

What SECURE 2.0 Means for Your Clients' Retirement and Estate Planning

SECURE 2.0 is here, but what does that mean for your clients' retirement and estate planning? On Tuesday, May 9, from 12 pm to 3 pm eastern, join NAIFA and the Society of Financial Service Professionals for an Advanced Practice Center live virtual event, as three industry experts discuss the impact of SECURE 2.0, what it means for your clients, and why now is the best time to prepare.

.png?width=300&name=_LUTCF%20%20-%20AT%20web%20(300%20x%20300%20px).png "_LUTCF - AT web (300 x 300 px)")