It’s easy to lose focus on interest rates when you’re helping your client search for a reverse mortgage loan.

After all, the interest rate won’t affect the monthly payment because they won’t have to make one (though they will need to pay taxes and insurance and maintain the home).

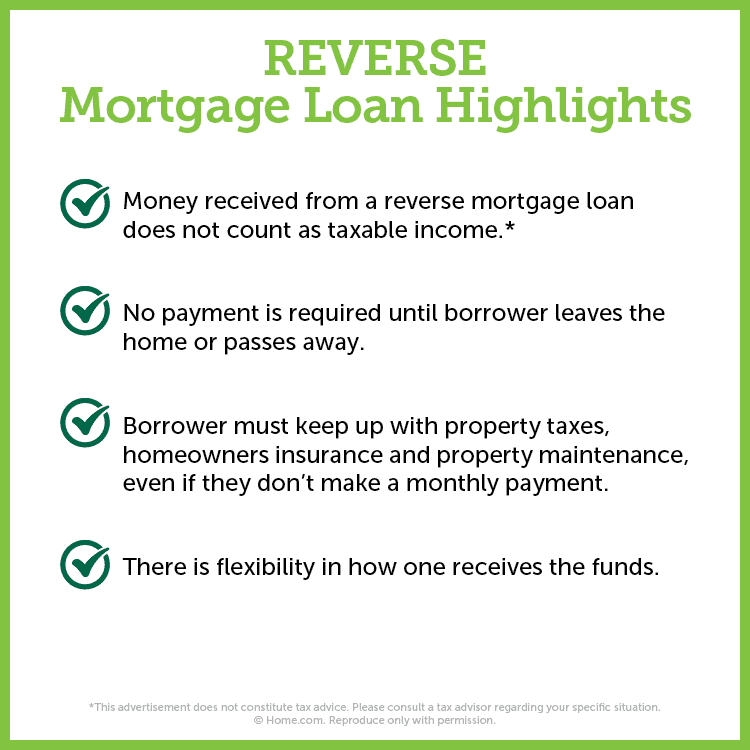

Reverse loans don’t require monthly payments, as the full balance comes due when the last borrower dies or leaves the home.

But reverse mortgage interest rates are still a big deal and should factor into your clients' borrowing decisions. The interest rate will make a huge difference when the balance comes due and your client or their heirs must decide what to do with the home.

What is a reverse mortgage?

Reverse mortgage loans aren’t all that complicated. But they are different from the traditional, or “forward,” mortgage loans with which most homeowners are familiar.

With a traditional mortgage the borrower builds equity, gradually, by making monthly payments. With a reverse mortgage, they can receive money by borrowing against the equity they’ve spent years building in their home.

Only homeowners 62 and older are eligible for reverse mortgages. The most common type of reverse mortgage (and what we’re referring to in this article) is a home equity conversion mortgage (HECM). HECMs are insured by the Federal Housing Administration (FHA), which is part of the U.S. Department of Housing and Urban Development (HUD).

Reverse home loans resemble the home equity loan or home equity line of credit (HELOC) some get to consolidate debt or renovate their house. The difference is reverse mortgages do not require ongoing monthly payments. The borrower does, however, have to pay taxes and insurance and maintain the home’s upkeep and repairs.

Instead, the loan balance becomes due when the last borrower moves, sells the home, or passes away.

The borrower can make payments, if they want, and doing so can keep their reverse loan balance from growing larger.

But they don’t have to. And that can be really helpful if your client is on a fixed income and needs access to more money each month.

A valuable source of retirement income

The combination of receiving payments from home equity and not owing a monthly mortgage payment can be a game-changer for your clients in retirement. Since they'll only need to pay taxes and insurance, plus any costs related to maintenance and upkeep, they can have more cash on hand for other expenses.

Even if your client is not retired yet, a reverse mortgage can significantly boost their retirement finances. Money received from a reverse mortgage does not count as taxable income, and they may be able to hold off on taking withdrawals from their investment accounts — which do count as taxable income — by relying on reverse funds instead.

Of course, everyone’s situation is unique, and you should talk with your clients to determine whether a reverse mortgage fits into their retirement financial plans.

How do reverse mortgage interest rates work?

A home's equity makes a reverse mortgage possible because the home serves as collateral and homeowners can borrow against the equity they've built. They can access the equity as a lump sum, a line of credit, monthly cash advances, or a combination of cash advances and a line of credit.

But even though they're receiving money, a reverse mortgage is still a loan. And loans come with costs.

Reverse mortgage costs

For a reverse loan, the costs come in the form of upfront closing costs, servicing fees, FHA mortgage insurance premiums (MIP), and — of course — interest.

Right now, we’re still in a relatively low interest rate environment. And if your client plans to remain in their home for the rest of their life, they may not be as concerned with your reverse mortgage interest rate as they would with a traditional mortgage or home equity loan.

They're not obligated to make a monthly mortgage payment, so they don’t have to worry about whether they can manage that cost. The only ongoing housing costs they'll have will be taxes, insurance, and any necessary maintenance and repairs on the home.

But it’s still important to consider the interest rate, especially if there’s a chance your client will want to sell the home and move elsewhere at some point in their retirement, or if they intend for their children to inherit the property and keep it in the family.

Although your client won’t owe a payment until the last borrower leaves the home, interest will accrue throughout the life of the loan. When the balance comes due, the borrower or their heirs will need to pay off the loan — whether that’s through the sale of the home, cash, or by refinancing to a forward mortgage.

Even if your client knows their heirs plan to sell the home when they inherit it, consider this. The higher the loan balance, the less money they’ll get to keep from the sale. They have to pay off the reverse mortgage lender before they get access to any of the profits.

That’s why it’s important to compare interest rates from at least three reputable reverse mortgage lenders and understand exactly how the interest will be charged.

How does interest accrue on a reverse mortgage?

When and how interest accrues on a reverse mortgage depends in part on how the funds are dispersed.

LUMP SUM

If your client receives their entire loan balance all at once, their lender will add the annual interest charges to the balance in monthly installments. Each month, their outstanding balance will grow a little larger if they choose not to make payments (again, they can make payments on a reverse mortgage, but they don’t have to. The borrower just needs to pay their property taxes and homeowners insurance and keep up with property maintenance).

LINE OF CREDIT

Your client can also set up a reverse mortgage line of credit and draw funds from it as needed. In this case, they would pay interest only on the amount used.

Another option is to receive monthly cash advances combined with a line of credit. You’ll want to discuss the terms of any of these plans with a reverse mortgage lender. The lump sum option may come with a fixed interest rate, so your client won't have to worry about the interest increasing substantially over time.

However, a lump sum disbursement may actually give your client access to a lower amount than a line of credit or monthly advances. And although the rate on a line of credit may be variable — meaning it can go up over time — your client may save money by not drawing on the funds until they absolutely need them.

This is why it’s critical to get quotes from several lenders. There are many options for how to best leverage a reverse mortgage, and the right one for your client will depend on their finances, goals, age, and the amount of equity they have in the home.

Whichever way your client chooses to receive the funds, though, shopping around for a competitive interest rate and making payments (if they can) can help keep the final loan balance in check for your client and their heirs.

To learn more about reverse mortgage disbursement options, see our guide here.

How can I get the best interest rate on a reverse mortgage?

To get the best reverse mortgage interest rate for your client, shop around. Getting a few quotes will give you a sense of what a reasonable rate looks like based on your client's circumstances, and if you get an outlier — either very high or low — you can ask the lender more detailed questions about the rate.

Some interest rate factors are beyond your client's control, such as their age, location, the appraised value of the home, and current market rates.

So, it’s important to control the factors you can influence, including shopping around and making an informed decision about how to structure the loan proceeds.

What types of reverse mortgage interest rates are there?

Reverse mortgage loans can come with different types of interest rates. The type of rate your client chooses will affect their long-term borrowing costs.

Fixed rate

Fixed-rate reverse mortgages have the same interest rate throughout the life of the loan. This means your client would be insulated from future rate increases, but won’t save money if rates drop significantly, as they did in 2020.

Typically, you’d get a fixed-rate reverse mortgage if you opt for a lump sum disbursement of the loan proceeds.

If your client needs to access a lot of equity all at once — to renovate their existing home for aging in place, for example — the fixed-rate, lump sum option may be the way to go. Or, if your client never wants to worry about the interest rate getting uncomfortably high, a fixed rate can bring peace of mind.

Adjustable Rate

Adjustable interest rate reverse mortgages have variable interest rates, which means the rate can change monthly or annually (either up or down).

If your client chooses to take a line of credit from their reverse mortgage, they'll have an adjustable rate loan. Interest will not be charged until they draw on the line of credit, and they have the option of paying it down whenever they choose.

As with the lump sum option, your client doesn’t have to pay on the line of credit. But if they want to keep drawing funds out, they can make payments to give themselves that flexibility.

Market conditions can cause the interest rate to rise, making the loan balance grow more quickly. However, there are caps on the amount of interest a lender can charge. Be sure to ask the reverse mortgage lender about whether the interest rate adjusts monthly or annually and what the relevant caps are.

A few reverse mortgage interest rate terms to know

As you and your client shop around for rates, you’ll probably see these reverse mortgage-specific terms. Here’s what they mean:

- Initial interest rate (IRR): This is your client's rate during the first month of an adjustable-rate reverse loan. It matters because it’s the basis for future rate fluctuations. This won’t apply if they're getting a fixed rate.

- Expected interest rate (EIR): Your client's ERR anticipates their variable rate loan’s reverse mortgage rate in 10 years, using their IRR as a starting point. If they're getting a fixed rate, their EIR will be the same as their IRR.

- Compounding rate: This rate combines the loan’s interest rate with the ongoing cost of your client's mortgage insurance premiums to measure their balance’s growth over time. (FHA mortgage insurance premiums add 0.5% of the loan amount each year and 2% upfront.)

Reverse mortgage interest rate FAQs

Monthly reverse mortgage payments are optional; the full loan balance comes due when the last borrower dies or moves out of the home.

Even though your client won't have to make a monthly mortgage payment, they will need to continue paying property taxes and homeowners insurance premiums. They'll also have to keep up with regular maintenance and repairs on the property.

Learn more

Reverse mortgage interest rates may seem like secondary thoughts since borrowers don’t have to worry about managing monthly payments on the principal and interest, and only need to stay current with their taxes, insurance, and maintenance.

But interest rates significantly impact the total loan balance your client and their heirs will need to pay off when they leave the home.

Fairway is not affiliated with any government agencies. These materials are not from HUD or FHA and were not approved by HUD or a government agency. Reverse mortgage borrowers are required to obtain an eligibility certificate by receiving counseling sessions with a HUD-approved agency. The youngest borrower must be at least 62 years old. Monthly reverse mortgage advances may affect eligibility for some other programs. This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Equal Housing Opportunity.

Some references sourced within this article have not been prepared by Fairway and are distributed for educational purposes only. The information is not guaranteed to be accurate and may not entirely represent the opinions of Fairway.

Based on research from leading reverse mortgage professionals Harlan Accola and Dan Hultquist

This article does not constitute tax or financial advice. Please consult a tax and/or financial advisor regarding your specific situation.

Fairway Independent Mortgage Corporation is a NAIFA partner.

.png?width=300&height=600&name=Tax%20Talk%20Graphic%20-%20email%20tower%20(300%20x%20600%20px).png)